import numpy as np

import pandas as pd

import torch

from torch import nn, optim

import statsmodels.api as sm

import matplotlib.pyplot as plt

from statsmodels.tsa.arima.model import ARIMAFitting Change of Slope Models via Pytorch: importance of scaling¶

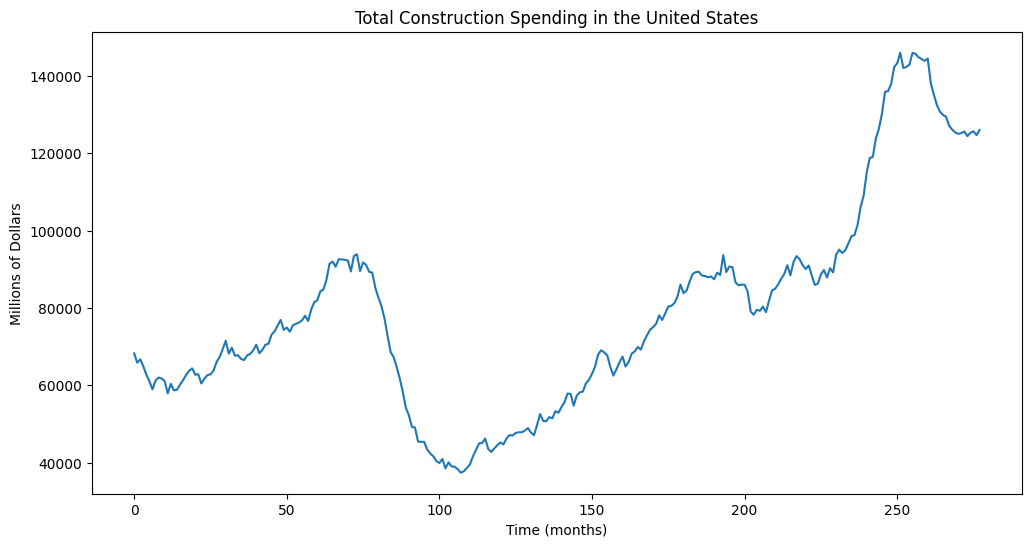

The following dataset is from \url{https://

ttlcons = pd.read_csv('TLCOMCONS_23April2025.csv')

print(ttlcons.head(10))

print(ttlcons.tail(10))

y_raw = ttlcons['TLCOMCONS']

n = len(y_raw)

x_raw = np.arange(1, n+1)

plt.figure(figsize = (12, 6))

plt.plot(y_raw)

plt.xlabel("Time (months)")

plt.ylabel('Millions of Dollars')

plt.title("Total Construction Spending in the United States")

plt.show() observation_date TLCOMCONS

0 2002-01-01 68254

1 2002-02-01 65840

2 2002-03-01 66722

3 2002-04-01 64879

4 2002-05-01 62741

5 2002-06-01 60982

6 2002-07-01 58971

7 2002-08-01 61223

8 2002-09-01 61997

9 2002-10-01 61772

observation_date TLCOMCONS

268 2024-05-01 126084

269 2024-06-01 125371

270 2024-07-01 124989

271 2024-08-01 125184

272 2024-09-01 125608

273 2024-10-01 124379

274 2024-11-01 125270

275 2024-12-01 125645

276 2025-01-01 124650

277 2025-02-01 125988

Let us try to fit the model:

where the unknown parameters are and (as well as σ which is the noise level in ). We will fix a value of . Here .

In PyTorch, this model can be coded as follows.

class PiecewiseLinearModel(nn.Module):

def __init__(self, knots_init, beta_init):

super().__init__()

self.num_knots = len(knots_init)

self.beta = nn.Parameter(torch.tensor(beta_init, dtype=torch.float32))

self.knots = nn.Parameter(torch.tensor(knots_init, dtype=torch.float32))

# When a tensor is wrapped in nn.Parameter and assigned as an attribute to a nn.Module,

# it is automatically registered as a parameter of that module.

def forward(self, x):

knots_sorted, _ = torch.sort(self.knots)

out = self.beta[0] + self.beta[1] * x

for j in range(self.num_knots):

out += self.beta[j + 2] * torch.relu(x - knots_sorted[j])

return outThe parameters will be estimated simply by least squares i.e., by minimizing

This is possibly a non-convex minimization problem (note that we are optimizing over as well). The algorithm used will be gradient descent (or a variant such as Adam). Initialization will be important for the algorithm to work well and not get stuck in bad local minima.

Here is how the least squares minimization is solved in PyTorch. The first step is to convert the data y_raw and x_raw into PyTorch tensors.

y_raw_torch = torch.tensor(y_raw, dtype=torch.float32)

x_raw_torch = torch.tensor(x_raw, dtype=torch.float32)The next step is to create suitable initialization. It is natural to take to be quantiles of at . For , we run a linear regression with these initial and then take the corresponding coefficients.

# First fix the number of knots

k = 4

quantile_levels = np.linspace(1/(k+1), k/(k+1), k)

knots_init = np.quantile(x_raw, quantile_levels)

n = len(y_raw)

X = np.column_stack([np.ones(n), x_raw])

for j in range(k):

xc = ((x_raw > knots_init[j]).astype(float)) * (x_raw - knots_init[j])

X = np.column_stack([X, xc])

md_init = sm.OLS(y_raw, X).fit()

beta_init = md_init.params.values

print(knots_init)

print(beta_init)[ 56.4 111.8 167.2 222.6]

[52167.91700846 628.19139706 -1505.22955093 1506.51113458

-264.69041849 565.3087544 ]

Note that the values of these initial coeffficients are on different scales (for example, the intercept is much larger in magnitude compared to the other terms).

Once the initial values are determined, we construct our model.

# Define a model

md_nn = PiecewiseLinearModel(knots_init=knots_init, beta_init=beta_init)

# This code creates an instance of our custom neural network class.

# It also initializes the knots at knots_init.Now we shall run the optimization algorithm which starts with these initial estimates, and then iteratively updates them. The crucial hyperparameter in the optimization algorithm is the learning rate (denoted by lr in the code below). This controls how much to adjust the parameters with respect to the gradient during each step of optimization. A smaller value means smaller steps, which can lead to more stable convergence but possibly slower training. A larger learning rate would update the parameters more aggressively, which might speed up training but risks overshooting the minimum.

# Define an optimizer

optimizer = optim.Adam(md_nn.parameters(), lr=1)

# Define a loss function

loss_fn = nn.MSELoss()

for epoch in range(300000):

# Zero gradients

optimizer.zero_grad()

# Without zeroing the gradients before each iteration,

# gradients from previous iterations would accumulate,

# leading to incorrect updates of the model's parameters.

# Compute loss

y_pred = md_nn(x_raw_torch)

loss = loss_fn(y_pred, y_raw_torch)

# Compute gradient

loss.backward()

# The .backward() method calculates the gradients of that tensor

# with respect to all the parameters in the network that contributed to its computation.

# Update parameters

optimizer.step()

# The .step() method performs a single optimization step,

# updating the model's parameters based on the gradients computed during the backward pass.

if epoch % 100 == 0:

print(f"Epoch {epoch}, Loss: {loss.item():.4f}")Here are some points that can be verified:

- When the learning rate is 0.01, the algorithm is moving too slowly and we get convergence after about 300000 epochs.

- When the learning rate is 0.1, the algorithm is still slow and convergence seems to be achieved at around 150000 epochs.

- When the learning rate is 1, the algorithm does not seem to settle down, and is oscillating quite a bit even after reaching around the smallest loss.

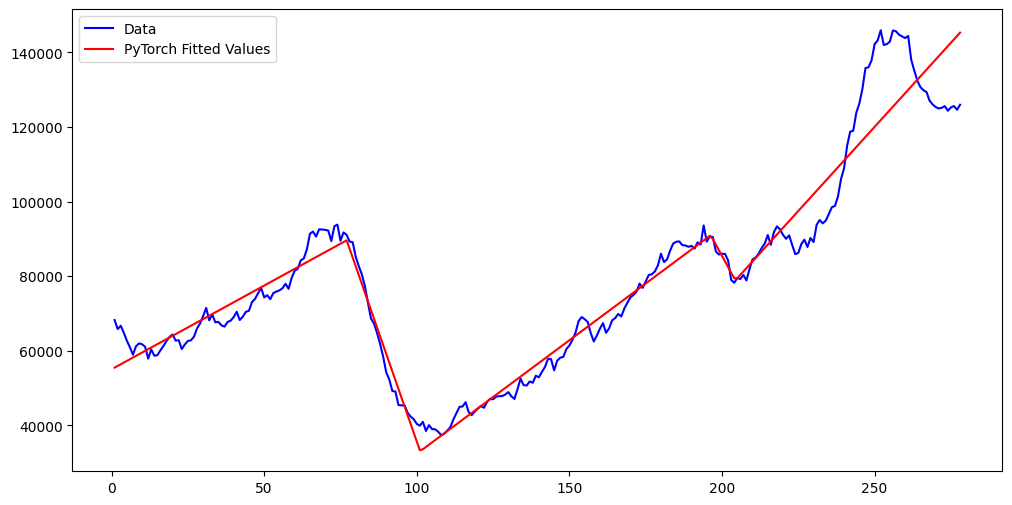

nn_fits = md_nn(x_raw_torch).detach().numpy()

# detach() in PyTorch creates a new tensor that shares the same storage as the original tensor

# but is detached from the computation graph.

plt.figure(figsize = (12, 6))

plt.plot(x_raw, y_raw, color = 'blue', label = 'Data')

plt.plot(x_raw, nn_fits, color = 'red', label = 'PyTorch Fitted Values')

plt.legend()

plt.show()

Now we shall scale the covariates and , and then run the same algorithm again.

y_scaled = (y_raw - np.mean(y_raw)) / (np.std(y_raw))

x_scaled = (x_raw - np.mean(x_raw)) / (np.std(x_raw))

y_torch = torch.tensor(y_scaled, dtype=torch.float32)

x_torch = torch.tensor(x_scaled, dtype=torch.float32)# First fix the number of knots

k = 4

quantile_levels = np.linspace(1/(k+1), k/(k+1), k)

knots_init = np.quantile(x_scaled, quantile_levels)

n = len(y_scaled)

X = np.column_stack([np.ones(n), x_scaled])

for j in range(k):

xc = ((x_scaled > knots_init[j]).astype(float)) * (x_scaled - knots_init[j])

X = np.column_stack([X, xc])

md_init = sm.OLS(y_scaled, X).fit()

beta_init = md_init.params.values

print(knots_init)

print(beta_init)[-1.03549894 -0.34516631 0.34516631 1.03549894]

[ 2.26579783 1.87350378 -4.48916248 4.49298465 -0.7894067 1.68596401]

Now the β coefficients are of the same scale.

md_nn = PiecewiseLinearModel(knots_init=knots_init, beta_init=beta_init)optimizer = optim.Adam(md_nn.parameters(), lr=0.01)

loss_fn = nn.MSELoss()

for epoch in range(20000):

# Zero gradients

optimizer.zero_grad()

# Compute loss

y_pred = md_nn(x_torch)

loss = loss_fn(y_pred, y_torch)

# Compute gradient

loss.backward()

# Update parameters

optimizer.step()

if epoch % 100 == 0:

print(f"Epoch {epoch}, Loss: {loss.item():.4f}")Epoch 0, Loss: 0.1118

Epoch 100, Loss: 0.0899

Epoch 200, Loss: 0.0809

Epoch 300, Loss: 0.0764

Epoch 400, Loss: 0.0739

Epoch 500, Loss: 0.0719

Epoch 600, Loss: 0.0704

Epoch 700, Loss: 0.0693

Epoch 800, Loss: 0.0684

Epoch 900, Loss: 0.0677

Epoch 1000, Loss: 0.0671

Epoch 1100, Loss: 0.0667

Epoch 1200, Loss: 0.0663

Epoch 1300, Loss: 0.0664

Epoch 1400, Loss: 0.0657

Epoch 1500, Loss: 0.0655

Epoch 1600, Loss: 0.0653

Epoch 1700, Loss: 0.0651

Epoch 1800, Loss: 0.0652

Epoch 1900, Loss: 0.0649

Epoch 2000, Loss: 0.0653

Epoch 2100, Loss: 0.0646

Epoch 2200, Loss: 0.0645

Epoch 2300, Loss: 0.0644

Epoch 2400, Loss: 0.0644

Epoch 2500, Loss: 0.0643

Epoch 2600, Loss: 0.0642

Epoch 2700, Loss: 0.0642

Epoch 2800, Loss: 0.0641

Epoch 2900, Loss: 0.0641

Epoch 3000, Loss: 0.0641

Epoch 3100, Loss: 0.0641

Epoch 3200, Loss: 0.0640

Epoch 3300, Loss: 0.0640

Epoch 3400, Loss: 0.0640

Epoch 3500, Loss: 0.0640

Epoch 3600, Loss: 0.0639

Epoch 3700, Loss: 0.0639

Epoch 3800, Loss: 0.0639

Epoch 3900, Loss: 0.0639

Epoch 4000, Loss: 0.0639

Epoch 4100, Loss: 0.0638

Epoch 4200, Loss: 0.0642

Epoch 4300, Loss: 0.0638

Epoch 4400, Loss: 0.0638

Epoch 4500, Loss: 0.0638

Epoch 4600, Loss: 0.0638

Epoch 4700, Loss: 0.0638

Epoch 4800, Loss: 0.0637

Epoch 4900, Loss: 0.0637

Epoch 5000, Loss: 0.0637

Epoch 5100, Loss: 0.0637

Epoch 5200, Loss: 0.0637

Epoch 5300, Loss: 0.0637

Epoch 5400, Loss: 0.0637

Epoch 5500, Loss: 0.0637

Epoch 5600, Loss: 0.0637

Epoch 5700, Loss: 0.0637

Epoch 5800, Loss: 0.0640

Epoch 5900, Loss: 0.0637

Epoch 6000, Loss: 0.0637

Epoch 6100, Loss: 0.0637

Epoch 6200, Loss: 0.0637

Epoch 6300, Loss: 0.0637

Epoch 6400, Loss: 0.0637

Epoch 6500, Loss: 0.0637

Epoch 6600, Loss: 0.0637

Epoch 6700, Loss: 0.0637

Epoch 6800, Loss: 0.0637

Epoch 6900, Loss: 0.0637

Epoch 7000, Loss: 0.0637

Epoch 7100, Loss: 0.0636

Epoch 7200, Loss: 0.0636

Epoch 7300, Loss: 0.0636

Epoch 7400, Loss: 0.0636

Epoch 7500, Loss: 0.0636

Epoch 7600, Loss: 0.0636

Epoch 7700, Loss: 0.0639

Epoch 7800, Loss: 0.0636

Epoch 7900, Loss: 0.0636

Epoch 8000, Loss: 0.0637

Epoch 8100, Loss: 0.0637

Epoch 8200, Loss: 0.0637

Epoch 8300, Loss: 0.0636

Epoch 8400, Loss: 0.0636

Epoch 8500, Loss: 0.0637

Epoch 8600, Loss: 0.0636

Epoch 8700, Loss: 0.0636

Epoch 8800, Loss: 0.0636

Epoch 8900, Loss: 0.0636

Epoch 9000, Loss: 0.0637

Epoch 9100, Loss: 0.0637

Epoch 9200, Loss: 0.0636

Epoch 9300, Loss: 0.0636

Epoch 9400, Loss: 0.0636

Epoch 9500, Loss: 0.0637

Epoch 9600, Loss: 0.0637

Epoch 9700, Loss: 0.0637

Epoch 9800, Loss: 0.0637

Epoch 9900, Loss: 0.0636

Epoch 10000, Loss: 0.0636

Epoch 10100, Loss: 0.0636

Epoch 10200, Loss: 0.0636

Epoch 10300, Loss: 0.0636

Epoch 10400, Loss: 0.0636

Epoch 10500, Loss: 0.0637

Epoch 10600, Loss: 0.0637

Epoch 10700, Loss: 0.0637

Epoch 10800, Loss: 0.0636

Epoch 10900, Loss: 0.0636

Epoch 11000, Loss: 0.0636

Epoch 11100, Loss: 0.0636

Epoch 11200, Loss: 0.0637

Epoch 11300, Loss: 0.0636

Epoch 11400, Loss: 0.0637

Epoch 11500, Loss: 0.0636

Epoch 11600, Loss: 0.0636

Epoch 11700, Loss: 0.0636

Epoch 11800, Loss: 0.0636

Epoch 11900, Loss: 0.0637

Epoch 12000, Loss: 0.0637

Epoch 12100, Loss: 0.0636

Epoch 12200, Loss: 0.0638

Epoch 12300, Loss: 0.0636

Epoch 12400, Loss: 0.0637

Epoch 12500, Loss: 0.0636

Epoch 12600, Loss: 0.0636

Epoch 12700, Loss: 0.0636

Epoch 12800, Loss: 0.0636

Epoch 12900, Loss: 0.0637

Epoch 13000, Loss: 0.0637

Epoch 13100, Loss: 0.0636

Epoch 13200, Loss: 0.0636

Epoch 13300, Loss: 0.0637

Epoch 13400, Loss: 0.0636

Epoch 13500, Loss: 0.0636

Epoch 13600, Loss: 0.0636

Epoch 13700, Loss: 0.0636

Epoch 13800, Loss: 0.0636

Epoch 13900, Loss: 0.0636

Epoch 14000, Loss: 0.0636

Epoch 14100, Loss: 0.0636

Epoch 14200, Loss: 0.0636

Epoch 14300, Loss: 0.0636

Epoch 14400, Loss: 0.0636

Epoch 14500, Loss: 0.0636

Epoch 14600, Loss: 0.0636

Epoch 14700, Loss: 0.0637

Epoch 14800, Loss: 0.0637

Epoch 14900, Loss: 0.0637

Epoch 15000, Loss: 0.0636

Epoch 15100, Loss: 0.0636

Epoch 15200, Loss: 0.0637

Epoch 15300, Loss: 0.0636

Epoch 15400, Loss: 0.0636

Epoch 15500, Loss: 0.0637

Epoch 15600, Loss: 0.0637

Epoch 15700, Loss: 0.0636

Epoch 15800, Loss: 0.0637

Epoch 15900, Loss: 0.0637

Epoch 16000, Loss: 0.0637

Epoch 16100, Loss: 0.0636

Epoch 16200, Loss: 0.0636

Epoch 16300, Loss: 0.0636

Epoch 16400, Loss: 0.0637

Epoch 16500, Loss: 0.0636

Epoch 16600, Loss: 0.0636

Epoch 16700, Loss: 0.0636

Epoch 16800, Loss: 0.0636

Epoch 16900, Loss: 0.0636

Epoch 17000, Loss: 0.0637

Epoch 17100, Loss: 0.0636

Epoch 17200, Loss: 0.0636

Epoch 17300, Loss: 0.0637

Epoch 17400, Loss: 0.0636

Epoch 17500, Loss: 0.0636

Epoch 17600, Loss: 0.0636

Epoch 17700, Loss: 0.0636

Epoch 17800, Loss: 0.0637

Epoch 17900, Loss: 0.0637

Epoch 18000, Loss: 0.0637

Epoch 18100, Loss: 0.0636

Epoch 18200, Loss: 0.0636

Epoch 18300, Loss: 0.0636

Epoch 18400, Loss: 0.0636

Epoch 18500, Loss: 0.0636

Epoch 18600, Loss: 0.0637

Epoch 18700, Loss: 0.0636

Epoch 18800, Loss: 0.0637

Epoch 18900, Loss: 0.0636

Epoch 19000, Loss: 0.0636

Epoch 19100, Loss: 0.0636

Epoch 19200, Loss: 0.0636

Epoch 19300, Loss: 0.0636

Epoch 19400, Loss: 0.0636

Epoch 19500, Loss: 0.0638

Epoch 19600, Loss: 0.0636

Epoch 19700, Loss: 0.0636

Epoch 19800, Loss: 0.0636

Epoch 19900, Loss: 0.0640

Now the convergence is much faster (after about 8000 iterations). Let us plot the fitted values on the original scale.

nn_fits_with_scaling = md_nn(x_torch).detach().numpy()

nn_fits_with_scaling_original_scale = (nn_fits_with_scaling * np.std(y_raw)) + np.mean(y_raw)

plt.figure(figsize = (12, 6))

plt.plot(x_raw, y_raw, color = 'blue', label = 'Data')

plt.plot(x_raw, nn_fits_with_scaling_original_scale, color = 'green', label = 'PyTorch Fitted Values (With Scaling)')

plt.plot(x_raw, nn_fits, color = 'red', label = 'PyTorch Fitted Values (Without Scaling)')

plt.legend()

plt.show()

The fit is quite close to what we got by running the code on the original raw data. But the convergence of the algorithm is much faster with scaling. This is why scaling is almost always recommended.

MA(1) and AR(1) model fitting via PyTorch¶

The algorithms from PyTorch can also be used to fit classical time series models. Here we illustrate how to fit MA(1) and AR(1) models.

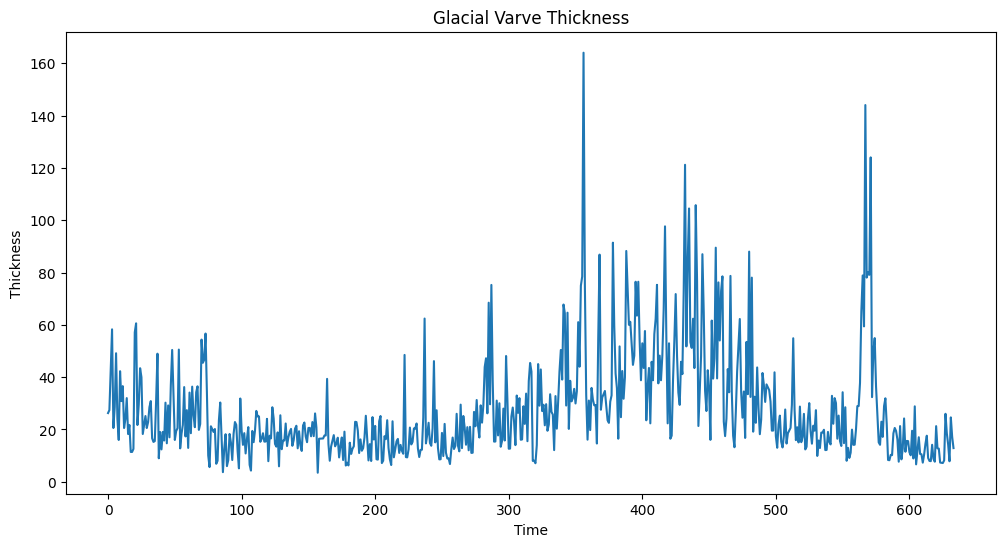

We will use the varve dataset from Lecture 20.

varve_data = pd.read_csv("varve.csv")

yraw = varve_data['x']

plt.figure(figsize = (12, 6))

plt.plot(yraw)

plt.xlabel('Time')

plt.ylabel('Thickness')

plt.title('Glacial Varve Thickness')

plt.show()

In Lecture 20, we took logarithms of this dataset, then differenced, and then fitted the MA(1) model. We will now fit this model (as well as AR(1)) using PyTorch (instead of ARIMA).

First let us recall how we fit this using ARIMA.

ylogdiff = np.diff(np.log(yraw))

mamod_ARIMA = ARIMA(ylogdiff, order=(0, 0, 1)).fit()

print(mamod_ARIMA.summary()) SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 633

Model: ARIMA(0, 0, 1) Log Likelihood -440.678

Date: Fri, 25 Apr 2025 AIC 887.356

Time: 10:50:24 BIC 900.707

Sample: 0 HQIC 892.541

- 633

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0013 0.004 -0.280 0.779 -0.010 0.008

ma.L1 -0.7710 0.023 -33.056 0.000 -0.817 -0.725

sigma2 0.2353 0.012 18.881 0.000 0.211 0.260

===================================================================================

Ljung-Box (L1) (Q): 9.16 Jarque-Bera (JB): 7.58

Prob(Q): 0.00 Prob(JB): 0.02

Heteroskedasticity (H): 0.95 Skew: -0.22

Prob(H) (two-sided): 0.69 Kurtosis: 3.30

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Below we describe the optimization problem that we need to solve in order to estimate the MA(1) parameters . Recall that the MA(1) model is given by

with . The likelihood is can be written in terms of the covariance matrix of . This is somewhat complicated. A simplification trick is to condition on , i.e., one attempts to write the conditional likelihood:

This likelihood is much simpler to write by breaking it down as

Each of the terms above can be written explicitly. Let and, for ,

Then

and

Thus the conditional likelihood given is given by

so that the negative log-likelihood becomes:

class MA1Model(nn.Module):

def __init__(self):

super().__init__()

self.mu = nn.Parameter(torch.tensor(0.0)) # initialized at 0

self.theta = nn.Parameter(torch.tensor(0.0)) # initialized at 0

self.log_sigma = nn.Parameter(torch.tensor(0.0)) # log(sigma)

def forward(self, y):

n = len(y)

eps_list = []

eps_prev = y[0] - self.mu # ε_0

eps_list.append(eps_prev)

for t in range(1, n):

eps_t = y[t] - self.mu - self.theta * eps_prev

eps_list.append(eps_t)

eps_prev = eps_t

eps = torch.stack(eps_list)

sigma = torch.exp(self.log_sigma)

nll = (0.5 * n * np.log(2 * np.pi)) + 0.5 * torch.sum(torch.log(sigma**2) + (eps**2) / (sigma**2))

return nllylogdiff_tensor = torch.tensor(ylogdiff, dtype=torch.float32) mamod = MA1Model()optimizer = optim.Adam(mamod.parameters(), lr=0.001)

for epoch in range(4000):

# Zero gradient

optimizer.zero_grad()

# Compute loss

loss = mamod(ylogdiff_tensor)

# Compute gradient

loss.backward()

# Update parameters

optimizer.step()

if epoch % 100 == 0:

sigma = torch.exp(mamod.log_sigma).item()

print(f"Epoch {epoch}, Loss: {loss.item():.4f}, mu: {mamod.mu.item():.4f}, "

f"theta: {mamod.theta.item():.4f}, sigma: {sigma:.4f}")

Epoch 0, Loss: 686.6678, mu: -0.0010, theta: -0.0010, sigma: 0.9990

Epoch 100, Loss: 637.9557, mu: -0.0011, theta: -0.1006, sigma: 0.9050

Epoch 200, Loss: 593.8228, mu: -0.0011, theta: -0.1994, sigma: 0.8229

Epoch 300, Loss: 554.7609, mu: -0.0010, theta: -0.2977, sigma: 0.7518

Epoch 400, Loss: 521.1600, mu: -0.0010, theta: -0.3950, sigma: 0.6909

Epoch 500, Loss: 493.3359, mu: -0.0010, theta: -0.4902, sigma: 0.6394

Epoch 600, Loss: 471.5909, mu: -0.0011, theta: -0.5805, sigma: 0.5968

Epoch 700, Loss: 456.2418, mu: -0.0010, theta: -0.6599, sigma: 0.5624

Epoch 800, Loss: 447.1696, mu: -0.0011, theta: -0.7199, sigma: 0.5359

Epoch 900, Loss: 442.9311, mu: -0.0011, theta: -0.7544, sigma: 0.5167

Epoch 1000, Loss: 441.2652, mu: -0.0011, theta: -0.7682, sigma: 0.5038

Epoch 1100, Loss: 440.6577, mu: -0.0011, theta: -0.7719, sigma: 0.4956

Epoch 1200, Loss: 440.4542, mu: -0.0011, theta: -0.7727, sigma: 0.4907

Epoch 1300, Loss: 440.3932, mu: -0.0011, theta: -0.7728, sigma: 0.4880

Epoch 1400, Loss: 440.3770, mu: -0.0011, theta: -0.7728, sigma: 0.4865

Epoch 1500, Loss: 440.3733, mu: -0.0011, theta: -0.7728, sigma: 0.4858

Epoch 1600, Loss: 440.3724, mu: -0.0011, theta: -0.7728, sigma: 0.4854

Epoch 1700, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4853

Epoch 1800, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 1900, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2000, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2100, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2200, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2300, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2400, Loss: 440.3724, mu: -0.0012, theta: -0.7728, sigma: 0.4852

Epoch 2500, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2600, Loss: 440.3723, mu: -0.0012, theta: -0.7728, sigma: 0.4852

Epoch 2700, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2800, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 2900, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3000, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3100, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3200, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3300, Loss: 440.3722, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3400, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3500, Loss: 440.3723, mu: -0.0012, theta: -0.7728, sigma: 0.4852

Epoch 3600, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3700, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3800, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

Epoch 3900, Loss: 440.3723, mu: -0.0011, theta: -0.7728, sigma: 0.4852

The following code prints out the estimates given by this code, with the estimates given by the ARIMA function.

ma1_pars = np.array([mamod.mu.detach().numpy(),

mamod.theta.detach().numpy(),

np.exp(2 * mamod.log_sigma.detach().numpy())])

# mu, theta and sigma^2

print(np.column_stack([mamod_ARIMA.params, ma1_pars]))

# the parameter estimates are quite close to each other[[-0.00125667 -0.00113865]

[-0.77099236 -0.77283102]

[ 0.23528045 0.23539422]]

Next let us fit the AR(1) model using PyTorch. Note that the full likelihood in the AR(1) model (stationary case) is given by (see Equation (6) in the notes for Lecture 17):

Below we first fit AR(1) using ARIMA, and then fit it by maximizing the log of the likelihood written above.

armod_ARIMA = ARIMA(ylogdiff, order=(1, 0, 0)).fit()

print(armod_ARIMA.summary()) SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 633

Model: ARIMA(1, 0, 0) Log Likelihood -494.562

Date: Fri, 25 Apr 2025 AIC 995.124

Time: 10:52:14 BIC 1008.475

Sample: 0 HQIC 1000.309

- 633

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const -0.0010 0.015 -0.067 0.946 -0.031 0.029

ar.L1 -0.3970 0.036 -10.989 0.000 -0.468 -0.326

sigma2 0.2793 0.015 18.916 0.000 0.250 0.308

===================================================================================

Ljung-Box (L1) (Q): 5.88 Jarque-Bera (JB): 5.22

Prob(Q): 0.02 Prob(JB): 0.07

Heteroskedasticity (H): 0.77 Skew: -0.17

Prob(H) (two-sided): 0.05 Kurtosis: 3.29

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

class AR1Model(nn.Module):

def __init__(self):

super().__init__()

# Learnable parameters: phi0 (intercept), phi1 (AR coefficient), log_sigma (for positivity)

self.phi0 = nn.Parameter(torch.tensor(0.0))

self.phi1 = nn.Parameter(torch.tensor(0.0))

self.log_sigma = nn.Parameter(torch.tensor(0.0)) # log(sigma) to ensure sigma > 0

def forward(self, y):

n = len(y)

sigma = torch.exp(self.log_sigma)

phi0 = self.phi0

phi1 = self.phi1

if torch.abs(phi1) >= 1:

return torch.tensor(float("inf")), None

# Stationary mean of y_1

y1_mean = phi0 / (1 - phi1)

# Compute log-likelihood parts

part1 = -0.5 * n * torch.log(torch.tensor(2 * torch.pi))

part2 = -n * torch.log(sigma)

part3 = 0.5 * torch.log(1 - phi1**2)

part4 = - (1 - phi1**2) / (2 * sigma**2) * (y[0] - y1_mean)**2

part5 = - (1 / (2 * sigma**2)) * torch.sum((y[1:] - phi0 - phi1 * y[:-1])**2)

negative_log_likelihood = -(part1 + part2 + part3 + part4 + part5)

return negative_log_likelihood

# Fit the model

armod = AR1Model()

optimizer = optim.Adam(armod.parameters(), lr=0.001)

for epoch in range(3000):

# Zero gradient

optimizer.zero_grad()

# Compute loss

loss = armod(ylogdiff_tensor)

# Compute gradient

loss.backward()

# Update parameters

optimizer.step()

if epoch % 100 == 0:

print(f"Epoch {epoch}: phi0={armod.phi0.item():.4f}, phi1={armod.phi1.item():.4f}, sigma={torch.exp(armod.log_sigma).item():.4f}, loss={loss.item():.4f}")Epoch 0: phi0=-0.0010, phi1=0.4990, sigma=0.9990, loss=754.7678

Epoch 100: phi0=-0.0008, phi1=0.3977, sigma=0.9057, loss=708.1990

Epoch 200: phi0=-0.0009, phi1=0.2938, sigma=0.8257, loss=664.1494

Epoch 300: phi0=-0.0010, phi1=0.1895, sigma=0.7572, loss=623.2971

Epoch 400: phi0=-0.0011, phi1=0.0874, sigma=0.6989, loss=586.7548

Epoch 500: phi0=-0.0011, phi1=-0.0099, sigma=0.6502, loss=555.8716

Epoch 600: phi0=-0.0012, phi1=-0.0992, sigma=0.6108, loss=531.7949

Epoch 700: phi0=-0.0011, phi1=-0.1778, sigma=0.5804, loss=514.9111

Epoch 800: phi0=-0.0013, phi1=-0.2431, sigma=0.5587, loss=504.4892

Epoch 900: phi0=-0.0014, phi1=-0.2943, sigma=0.5445, loss=498.8905

Epoch 1000: phi0=-0.0014, phi1=-0.3318, sigma=0.5362, loss=496.2641

Epoch 1100: phi0=-0.0014, phi1=-0.3575, sigma=0.5318, loss=495.1721

Epoch 1200: phi0=-0.0014, phi1=-0.3742, sigma=0.5298, loss=494.7625

Epoch 1300: phi0=-0.0015, phi1=-0.3844, sigma=0.5289, loss=494.6224

Epoch 1400: phi0=-0.0014, phi1=-0.3904, sigma=0.5286, loss=494.5786

Epoch 1500: phi0=-0.0014, phi1=-0.3936, sigma=0.5285, loss=494.5660

Epoch 1600: phi0=-0.0014, phi1=-0.3954, sigma=0.5285, loss=494.5628

Epoch 1700: phi0=-0.0014, phi1=-0.3962, sigma=0.5285, loss=494.5621

Epoch 1800: phi0=-0.0015, phi1=-0.3967, sigma=0.5285, loss=494.5620

Epoch 1900: phi0=-0.0014, phi1=-0.3968, sigma=0.5285, loss=494.5618

Epoch 2000: phi0=-0.0014, phi1=-0.3969, sigma=0.5285, loss=494.5619

Epoch 2100: phi0=-0.0014, phi1=-0.3969, sigma=0.5285, loss=494.5619

Epoch 2200: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5619

Epoch 2300: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5619

Epoch 2400: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5618

Epoch 2500: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5619

Epoch 2600: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5618

Epoch 2700: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5618

Epoch 2800: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5619

Epoch 2900: phi0=-0.0014, phi1=-0.3970, sigma=0.5285, loss=494.5619

ar1_pars = np.array([armod.phi0.detach().numpy(),

armod.phi1.detach().numpy(),

np.exp(2 * armod.log_sigma.detach().numpy())])

# mu, theta and sigma^2

print(np.column_stack([armod_ARIMA.params, ar1_pars]))[[-0.00102183 -0.00127035]

[-0.39696193 -0.39696154]

[ 0.27927876 0.27927745]]

It is possible to extend these methods to fit AR() and MA() for more general and using PyTorch. The PyTorch seems to work just as well as ARIMA. In the above, the PyTorch seems to take much longer time but this is only because we are running the method for a few thousand epochs. The actual convergence seems to have happened much earlier.