import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

from statsmodels.tsa.ar_model import AutoReg

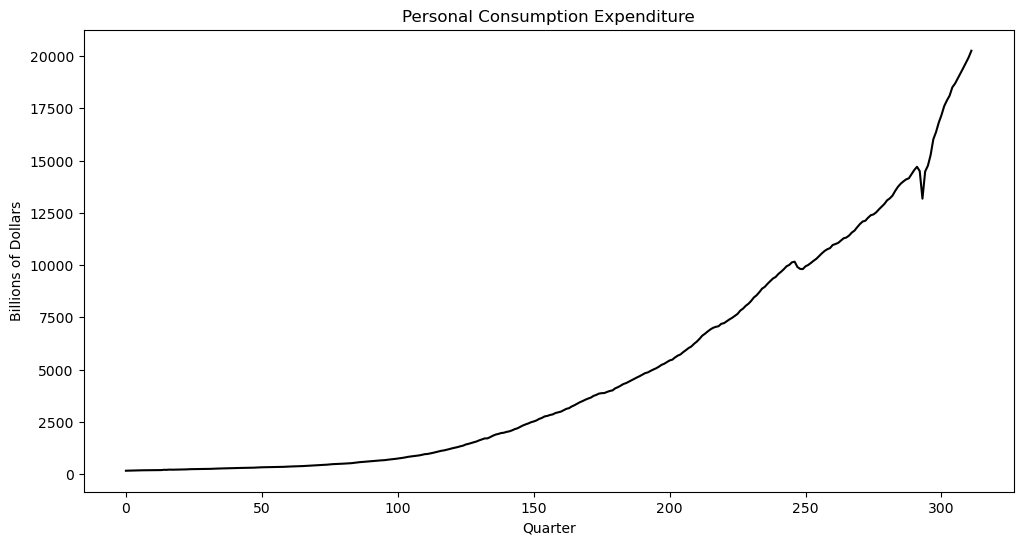

from scipy import statsThe following data is on personal consumption expenditures from FRED (https://

pcec = pd.read_csv("PCEC_03April2025.csv")

print(pcec.head())

y = pcec['PCEC']

plt.figure(figsize = (12, 6))

plt.plot(y, color = 'black')

plt.xlabel('Quarter')

plt.ylabel('Billions of Dollars')

plt.title('Personal Consumption Expenditure')

plt.show() observation_date PCEC

0 1947-01-01 156.161

1 1947-04-01 160.031

2 1947-07-01 163.543

3 1947-10-01 167.672

4 1948-01-01 170.372

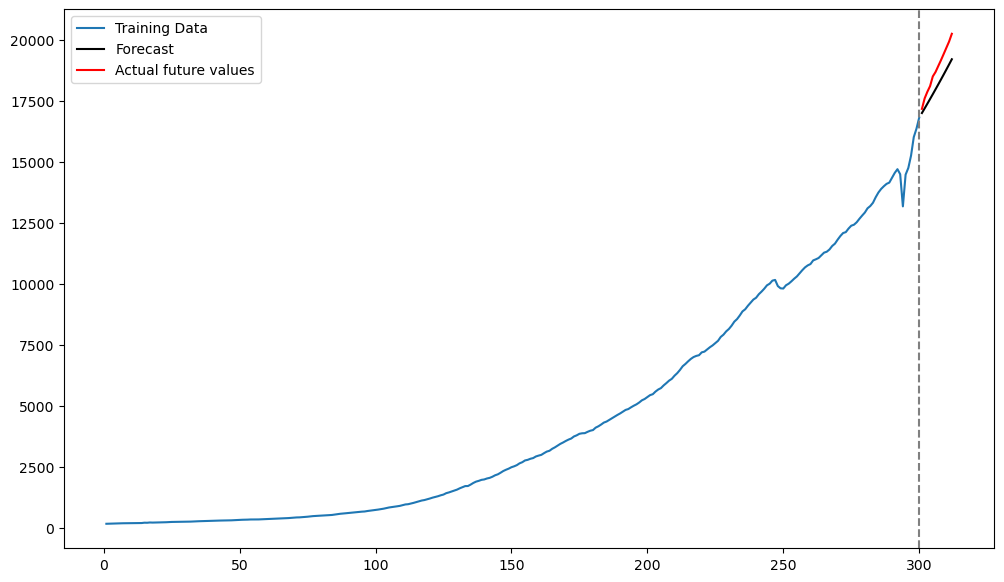

We will fit AR(p) models to this dataset, and use the fitted models to predict future values. Let us leave the last 12 observations (corresponding to three years) as test values, and the remaining data form the training data. We will fit AR(p) models to the training data, predict the test values and then compare the predictions with the actual test values.

n = len(y)

tme = range(1, n+1)

n_test = 12

n_train = n - n_test

y_train = y[:n_train]

tme_train = tme[:n_train]

y_test = y[n_train:]

tme_test = tme[n_train:]Below, we fit AR(p) to the training data.

p = 1 #for selecting p, some heuristics can be used (one such method will be detailed in the lab tomorrow)

armod_sm = AutoReg(y_train, lags = p).fit()

print(armod_sm.summary()) AutoReg Model Results

==============================================================================

Dep. Variable: PCEC No. Observations: 300

Model: AutoReg(1) Log Likelihood -1866.593

Method: Conditional MLE S.D. of innovations 124.443

Date: Thu, 03 Apr 2025 AIC 3739.187

Time: 15:46:12 BIC 3750.288

Sample: 1 HQIC 3743.630

300

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 9.3717 9.975 0.940 0.347 -10.178 28.922

PCEC.L1 1.0106 0.002 638.038 0.000 1.008 1.014

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 0.9895 +0.0000j 0.9895 0.0000

-----------------------------------------------------------------------------

Here is how the fitted model can be used to predict the test observations.

k = n_test

fcast = armod_sm.get_prediction(start = n_train, end = n_train+k-1)

fcast_mean = fcast.predicted_mean #this gives the point predictions: the fitted model's best estimate (expected value) of the future values of the time series The method that the above function uses to calculate the predictions was detailed in class; and is captured in the code below.

#Predictions

yhat = np.concatenate([y_train.astype(float), np.full(k, -9999)]) #extend data by k placeholder values

phi_vals = armod_sm.params

for i in range(1, k+1):

ans = phi_vals.iloc[0]

for j in range(1, p+1):

ans += phi_vals.iloc[j] * yhat[n_train+i-j-1]

yhat[n_train+i-1] = ans

predvalues = yhat[n_train:]

#Check that both predictions are identical:

print(np.column_stack([predvalues, fcast_mean]))[[17004.24661408 17004.24661408]

[17194.3607461 17194.3607461 ]

[17386.49564942 17386.49564942]

[17580.67280334 17580.67280334]

[17776.91391546 17776.91391546]

[17975.24092412 17975.24092412]

[18175.67600083 18175.67600083]

[18378.2415528 18378.2415528 ]

[18582.96022537 18582.96022537]

[18789.85490462 18789.85490462]

[18998.94871987 18998.94871987]

[19210.26504629 19210.26504629]]

Below we plot the predictions along with the actual test observations.

plt.figure(figsize = (12, 7))

plt.plot(tme_train, y_train, label = 'Training Data')

plt.plot(tme_test, fcast_mean, label = 'Forecast', color = 'black')

plt.plot(tme_test, y_test, color = 'red', label = 'Actual future values')

plt.axvline(x=n_train, color='gray', linestyle='--')

plt.legend()

plt.show()

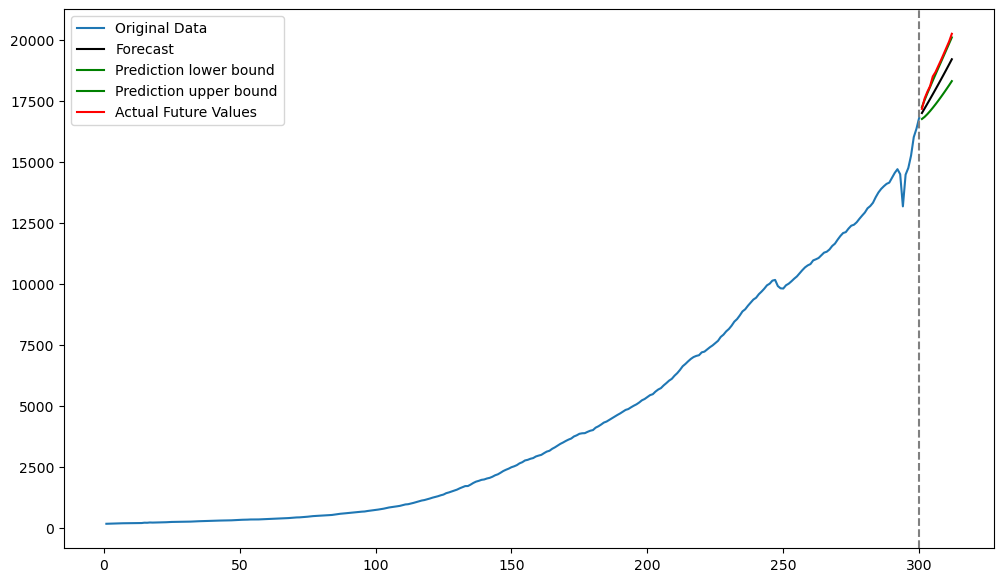

Next we discuss prediction uncertainty quantification. The prediction standard errors, and the associated uncertainty intervals, are calculated as follows.

fcast_se = fcast.se_mean

alpha = 0.05

z_alpha_half = stats.norm.ppf(1 - alpha/2)

predlower = predvalues - z_alpha_half * fcast_se

predupper = predvalues + z_alpha_half * fcast_se

fcast_int = fcast.conf_int()

print(np.column_stack([predlower, predupper, fcast_int]))

[[16760.34256946 17248.15065871 16760.34256946 17248.15065871]

[16847.5903057 17541.13118649 16847.5903057 17541.13118649]

[16959.51925994 17813.47203889 16959.51925994 17813.47203889]

[17084.99727308 18076.3483336 17084.99727308 18076.3483336 ]

[17219.74763362 18334.08019731 17219.74763362 18334.08019731]

[17361.59779426 18588.88405398 17361.59779426 18588.88405398]

[17509.27171192 18842.08028975 17509.27171192 18842.08028975]

[17661.94913809 19094.5339675 17661.94913809 19094.5339675 ]

[17819.06940933 19346.85104141 17819.06940933 19346.85104141]

[17980.23199936 19599.47780988 17980.23199936 19599.47780988]

[18145.14124017 19852.75619956 18145.14124017 19852.75619956]

[18313.57338418 20106.95670841 18313.57338418 20106.95670841]]

Below we plot the predictions along with uncertainty intervals.

#Plotting predictions along with uncertainty:

plt.figure(figsize = (12, 7))

plt.plot(tme_train, y_train, label = 'Original Data')

plt.plot(tme_test, predvalues, label = 'Forecast', color = 'black')

plt.plot(tme_test, predlower, color = 'green', label = 'Prediction lower bound')

plt.plot(tme_test, predupper, color = 'green', label = 'Prediction upper bound')

plt.plot(tme_test, y_test, color = 'red', label = 'Actual Future Values')

plt.legend()

plt.axvline(x=n_train, color='gray', linestyle='--')

plt.show()

In this example, the predicted values are somewhat below the actual test values. The upper 95% interval values are almost coinciding with the actual test values.

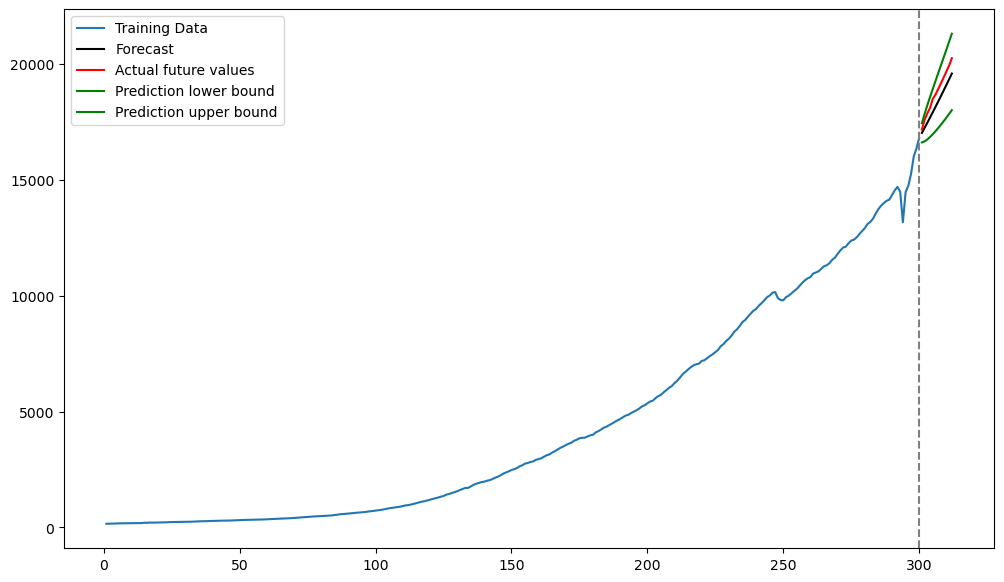

Instead of applying AR models, directly to the raw data, it is common practice to apply them to the logarithms.

ylog_train = np.log(y_train)

ylog_test = np.log(y_test)p = 1

armod_sm = AutoReg(ylog_train, lags = p).fit()

print(armod_sm.summary()) AutoReg Model Results

==============================================================================

Dep. Variable: PCEC No. Observations: 300

Model: AutoReg(1) Log Likelihood 886.697

Method: Conditional MLE S.D. of innovations 0.012

Date: Thu, 03 Apr 2025 AIC -1767.395

Time: 15:56:11 BIC -1756.293

Sample: 1 HQIC -1762.952

300

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0255 0.004 6.726 0.000 0.018 0.033

PCEC.L1 0.9987 0.000 2031.123 0.000 0.998 1.000

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.0013 +0.0000j 1.0013 0.0000

-----------------------------------------------------------------------------

Predictions are obtained as follows.

fcast = armod_sm.get_prediction(start = n_train, end = n_train+k-1)

fcast_mean = fcast.predicted_mean #this gives the point predictionsPrediction uncertainty intervals are obtained as follows.

fcast_se = fcast.se_mean

alpha = 0.05

z_alpha_half = stats.norm.ppf(1 - alpha/2)

predlower = fcast_mean - z_alpha_half * fcast_se

predupper = fcast_mean + z_alpha_half * fcast_se

fcast_int = fcast.conf_int()

print(np.column_stack([predlower, predupper, fcast_int]))[[9.71848283 9.76736179 9.71848283 9.76736179]

[9.72119381 9.79027425 9.72119381 9.79027425]

[9.72625359 9.81080467 9.72625359 9.81080467]

[9.73252367 9.83009157 9.73252367 9.83009157]

[9.73956275 9.84857632 9.73956275 9.84857632]

[9.74714436 9.86648543 9.74714436 9.86648543]

[9.75513388 9.88395354 9.75513388 9.88395354]

[9.76344355 9.90106847 9.76344355 9.90106847]

[9.77201237 9.91789126 9.77201237 9.91789126]

[9.78079591 9.93446638 9.78079591 9.93446638]

[9.78976061 9.95082743 9.78976061 9.95082743]

[9.79888039 9.96700055 9.79888039 9.96700055]]

plt.figure(figsize = (12, 7))

plt.plot(tme_train, y_train, label = 'Training Data')

plt.plot(tme_test, np.exp(fcast_mean), label = 'Forecast', color = 'black') #Note the exponentiation

plt.plot(tme_test, y_test, color = 'red', label = 'Actual future values')

plt.plot(tme_test, np.exp(predlower), color = 'green', label = 'Prediction lower bound')

plt.plot(tme_test, np.exp(predupper), color = 'green', label = 'Prediction upper bound')

plt.axvline(x=n_train, color='gray', linestyle='--')

plt.legend()

plt.show()

Now the predictions are more accurate.

How are the Prediction Uncertainties actually calculated?¶

We now calculate the prediction standard errors directly using the method described in class. The first step is to fit the AR(p) model and then to obtain estimates of as well as σ. There are two estimates of σ (only difference being the denominators: vs ).

yreg = ylog_train[p:] #these are the response values in the autoregression

Xmat = np.ones((n_train-p, 1)) #this will be the design matrix (X) in the autoregression

for j in range(1, p+1):

col = ylog_train[p-j : n_train-j]

Xmat = np.column_stack([Xmat, col])

armod = sm.OLS(yreg, Xmat).fit()

print(armod.params)

print(armod.summary())

sighat = np.sqrt(np.mean(armod.resid ** 2)) #note that this mean is taken over n-p observations

resdf = n_train - 2*p - 1

sigols = np.sqrt((np.sum(armod.resid ** 2))/resdf)

print(sighat, sigols)const 0.025454

x1 0.998702

dtype: float64

OLS Regression Results

==============================================================================

Dep. Variable: PCEC R-squared: 1.000

Model: OLS Adj. R-squared: 1.000

Method: Least Squares F-statistic: 4.098e+06

Date: Thu, 03 Apr 2025 Prob (F-statistic): 0.00

Time: 16:42:25 Log-Likelihood: 886.70

No. Observations: 299 AIC: -1769.

Df Residuals: 297 BIC: -1762.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0255 0.004 6.703 0.000 0.018 0.033

x1 0.9987 0.000 2024.318 0.000 0.998 1.000

==============================================================================

Omnibus: 145.321 Durbin-Watson: 1.957

Prob(Omnibus): 0.000 Jarque-Bera (JB): 7908.842

Skew: -1.144 Prob(JB): 0.00

Kurtosis: 28.092 Cond. No. 41.1

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

0.012469349713719 0.012511263612463488

The two estimates of σ lead to two values for standard errors.

covmat = (sighat ** 2) * np.linalg.inv(np.dot(Xmat.T, Xmat))

covmat_ols = (sigols ** 2) * np.linalg.inv(np.dot(Xmat.T, Xmat))

print(np.sqrt(np.diag(covmat)))

print(np.sqrt(np.diag(covmat_ols)))

print(armod_sm.bse)

print(armod.bse)[0.00378458 0.0004917 ]

[0.0037973 0.00049335]

const 0.003785

PCEC.L1 0.000492

dtype: float64

const 0.003797

x1 0.000493

dtype: float64

The following code computes the prediction standard errors. It uses the matrix recursion method described in class.

sigest = sighat

Gamhat = np.array([[sigest ** 2]])

vkp = np.array([[armod.params.iloc[1]]])

for i in range(1, k):

covterm = Gamhat @ vkp

varterm = sigest**2 + (vkp.T @ (Gamhat @ vkp))

Gamhat = np.block([

[Gamhat, covterm],

[covterm.T, varterm ]

])

if i < p:

new_coef = armod.params.iloc[i+1]

vkp = np.vstack([ [new_coef], vkp ])

else:

vkp = np.vstack([ [0], vkp ])

predsd = np.sqrt(np.diag(Gamhat))

#Check that this method produces the same standard errors as those computed by .se_mean:

print(np.column_stack([predsd, fcast_se]))[[0.01246935 0.01246935]

[0.01762289 0.01762289]

[0.02156955 0.02156955]

[0.02489023 0.02489023]

[0.0278101 0.0278101 ]

[0.03044471 0.03044471]

[0.03286276 0.03286276]

[0.03510904 0.03510904]

[0.03721469 0.03721469]

[0.03920237 0.03920237]

[0.04108923 0.04108923]

[0.04288859 0.04288859]]