We illustrate how to use the estimators and as well as and for estimating smooth trends in time series data.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

import cvxpy as cpWe will use the following two functions (based on the python convex optimization library cvxpy) for computing the ridge and lasso estimators.

#below penalty_start = 2 means that b0 and b1 are not included in the penalty

def solve_ridge(X, y, lambda_val, penalty_start=2):

n, p = X.shape

# Define variable

beta = cp.Variable(p)

# Define objective

loss = cp.sum_squares(X @ beta - y)

reg = lambda_val * cp.sum_squares(beta[penalty_start:])

objective = cp.Minimize(loss + reg)

# Solve problem

prob = cp.Problem(objective)

prob.solve()

return beta.value#below penalty_start = 2 means that b0 and b1 are not included in the penalty

def solve_lasso(X, y, lambda_val, penalty_start=2):

n, p = X.shape

# Define variable

beta = cp.Variable(p)

# Define objective

loss = cp.sum_squares(X @ beta - y)

reg = lambda_val * cp.norm1(beta[penalty_start:])

objective = cp.Minimize(loss + reg)

# Solve problem

prob = cp.Problem(objective)

prob.solve()

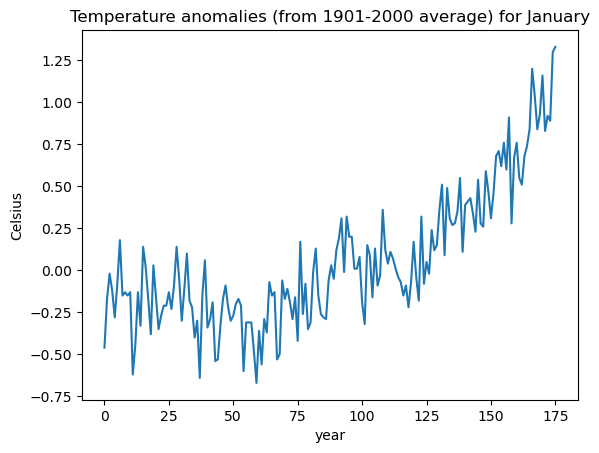

return beta.valueThe following dataset is from NOAA climate at a glance. It contains temperature anomalies for the month of January. Anomalies are in celsius and are with respect to the 1901-2000 average.

temp_jan = pd.read_csv('TempAnomalies_January_Feb2025.csv', skiprows=4)

print(temp_jan.head())

y = temp_jan['Anomaly']

plt.plot(y)

plt.xlabel('year')

plt.ylabel('Celsius')

plt.title('Temperature anomalies (from 1901-2000 average) for January')

plt.show() Year Anomaly

0 1850 -0.46

1 1851 -0.17

2 1852 -0.02

3 1853 -0.12

4 1854 -0.28

The matrix in the representation of this model is constructed as follows.

n = len(y)

x = np.arange(1, n+1)

Xfull = np.column_stack([np.ones(n), x-1])

for i in range(n-2):

c = i+2

xc = ((x > c).astype(float))*(x-c)

Xfull = np.column_stack([Xfull, xc])

print(Xfull)[[ 1. 0. -0. ... -0. -0. -0.]

[ 1. 1. 0. ... -0. -0. -0.]

[ 1. 2. 1. ... -0. -0. -0.]

...

[ 1. 173. 172. ... 1. 0. -0.]

[ 1. 174. 173. ... 2. 1. 0.]

[ 1. 175. 174. ... 3. 2. 1.]]

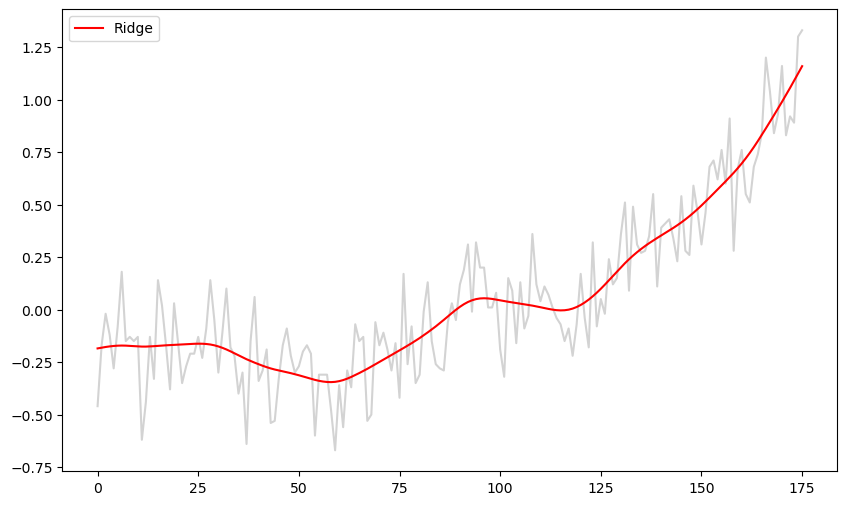

The ridge regression estimate is computed below. Start with some standard choice of λ (e.g., ) and then increase or decrease it by factors of 10 until you get a fit that is visually nice (smooth while capturing patterns in the data).

b_ridge = solve_ridge(Xfull, y, lambda_val = 1000)

ridge_fitted = np.dot(Xfull, b_ridge)

plt.figure(figsize = (10, 6))

plt.plot(y, color = 'lightgray')

plt.plot(ridge_fitted, color = 'red', label = 'Ridge')

plt.legend()

plt.show()

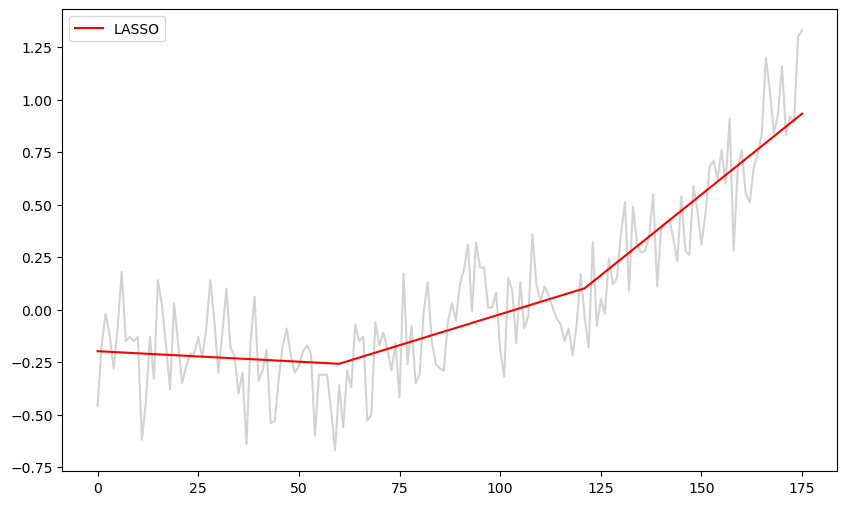

The code for LASSO is given below. Start with some standard choice of λ (e.g., ) and then increase or decrease it by factors of 10 until you get a fit that is visually nice.

b_lasso = solve_lasso(Xfull, y, lambda_val = 100)

lasso_fitted = np.dot(Xfull, b_lasso)

plt.figure(figsize = (10, 6))

plt.plot(y, color = 'lightgray')

plt.plot(lasso_fitted, color = 'red', label = 'LASSO')

plt.legend()

plt.show()

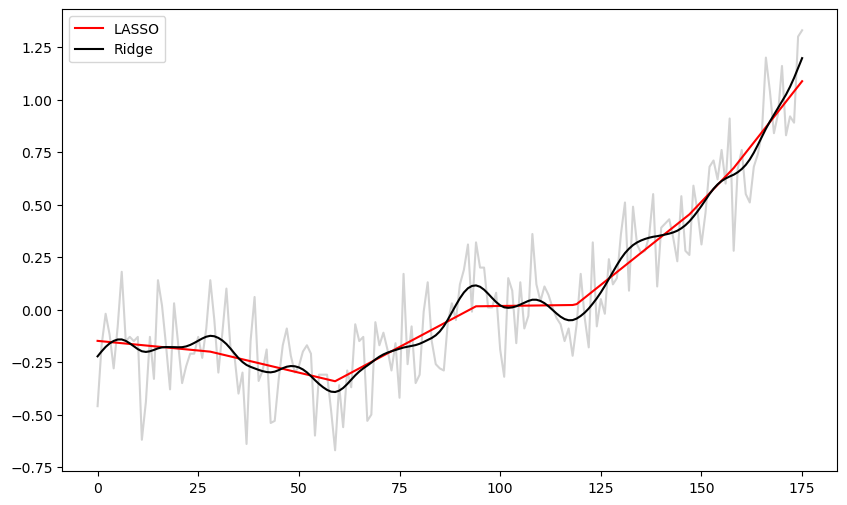

Note that the LASSO fit is piecewise linear while the ridge fit is more smoother (without any kinks).

b_ridge = solve_ridge(Xfull, y, lambda_val = 100)

ridge_fitted = np.dot(Xfull, b_ridge)

b_lasso = solve_lasso(Xfull, y, lambda_val = 10)

lasso_fitted = np.dot(Xfull, b_lasso)

plt.figure(figsize=(10, 6))

plt.plot(y, color = 'lightgray')

#plt.plot(y, color = 'None')

plt.plot(lasso_fitted, color = 'red', label = 'LASSO')

plt.plot(ridge_fitted, color = 'black', label = "Ridge")

plt.legend()

plt.show()

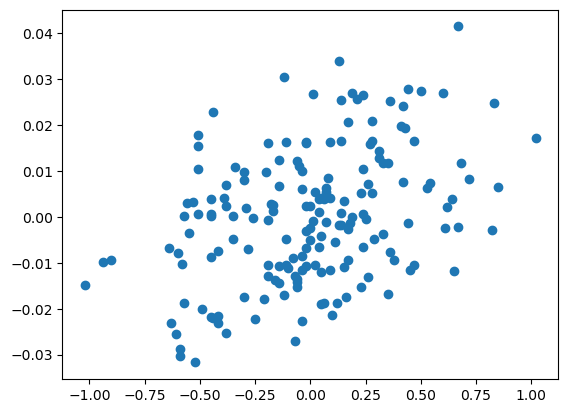

We compare the ridge estimates for β with unregularized estimates (which correspond to ) below.

b_ridge_0 = solve_ridge(Xfull, y, lambda_val = 0)

b_ridge = solve_ridge(Xfull, y, lambda_val = 10)

plt.scatter(b_ridge_0[2:], b_ridge[2:])

print(b_ridge_0[1], b_ridge[1])

print(b_ridge_0[0], b_ridge[0])0.28999999999997206 0.08093800016168097

-0.4599999999999922 -0.31625538257232577

Note that the -axis has a much tighter range compared to the -axis. This illustrates the shrinkage aspect of ridge regression.

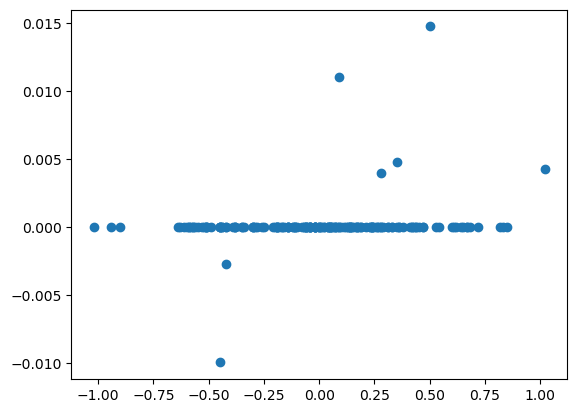

Below we compare the LASSO estimates with the unregularized MLE (which corresponds to ).

b_lasso_0 = solve_lasso(Xfull, y, lambda_val = 0)

b_lasso = solve_lasso(Xfull, y, lambda_val = 10)

plt.scatter(b_lasso_0[2:], b_lasso[2:])

plt.show()

print(b_lasso_0[1], b_lasso[1])

print(b_lasso_0[0], b_lasso[0])

0.290000000000026 -0.0018357831169318211

-0.4599999999999873 -0.14899519332692415

This plot clearly shows that the LASSO sets most coefficients exactly to zero. Compare this plot to the corresponding plot for the ridge estimator.

The following code implements cross validation for selecting λ in ridge regression.

def ridge_cv(X, y, lambda_candidates):

n = len(y)

folds = []

for i in range(5):

test_indices = np.arange(i, n, 5)

train_indices = np.array([j for j in range(n) if j % 5 != i])

folds.append((train_indices, test_indices))

cv_errors = {lamb: 0 for lamb in lambda_candidates}

for train_index, test_index in folds:

X_train = X[train_index]

X_test = X[test_index]

y_train = y[train_index]

y_test = y[test_index]

for lamb in lambda_candidates:

beta = solve_ridge(X_train, y_train, lambda_val = lamb)

y_pred = np.dot(X_test, beta)

squared_errors = (y_test - y_pred) ** 2

cv_errors[lamb] += np.sum(squared_errors)

for lamb in lambda_candidates:

cv_errors[lamb] /= n

best_lambda = min(cv_errors, key = cv_errors.get)

return best_lambda, cv_errorslambda_candidates = np.array([0.1, 1, 10, 100, 1000, 10000, 100000])

print(lambda_candidates)

best_lambda, cv_errors = ridge_cv(Xfull, y, lambda_candidates)

print(best_lambda)

print("CV errors for each lambda:")

for lamb, error in sorted(cv_errors.items()):

print(f"Lambda = {lamb:.2f}, CV Error = {error:.6f}")

[1.e-01 1.e+00 1.e+01 1.e+02 1.e+03 1.e+04 1.e+05]

100.0

CV errors for each lambda:

Lambda = 0.10, CV Error = 0.038557

Lambda = 1.00, CV Error = 0.034160

Lambda = 10.00, CV Error = 0.030811

Lambda = 100.00, CV Error = 0.030621

Lambda = 1000.00, CV Error = 0.030640

Lambda = 10000.00, CV Error = 0.031044

Lambda = 100000.00, CV Error = 0.033401

The following code illustrated cross validation for selecting λ in LASSO.

def lasso_cv(X, y, lambda_candidates):

n = len(y)

folds = []

for i in range(5):

test_indices = np.arange(i, n, 5)

train_indices = np.array([j for j in range(n) if j % 5 != i])

folds.append((train_indices, test_indices))

cv_errors = {lamb: 0 for lamb in lambda_candidates}

for train_index, test_index in folds:

X_train = X[train_index]

X_test = X[test_index]

y_train = y[train_index]

y_test = y[test_index]

for lamb in lambda_candidates:

beta = solve_lasso(X_train, y_train, lambda_val = lamb)

y_pred = np.dot(X_test, beta)

squared_errors = (y_test - y_pred) ** 2

cv_errors[lamb] += np.sum(squared_errors)

for lamb in lambda_candidates:

cv_errors[lamb] /= n

best_lambda = min(cv_errors, key = cv_errors.get)

return best_lambda, cv_errorslambda_candidates = np.array([0.1, 1, 10, 100, 1000, 10000, 100000])

print(lambda_candidates)

best_lambda, cv_errors = lasso_cv(Xfull, y, lambda_candidates)

print(best_lambda)

print("CV errors for each lambda:")

for lamb, error in sorted(cv_errors.items()):

print(f"Lambda = {lamb:.2f}, CV Error = {error:.6f}")

[1.e-01 1.e+00 1.e+01 1.e+02 1.e+03 1.e+04 1.e+05]

10.0

CV errors for each lambda:

Lambda = 0.10, CV Error = 0.034315

Lambda = 1.00, CV Error = 0.031163

Lambda = 10.00, CV Error = 0.030645

Lambda = 100.00, CV Error = 0.034554

Lambda = 1000.00, CV Error = 0.066568

Lambda = 10000.00, CV Error = 0.066568

Lambda = 100000.00, CV Error = 0.066568

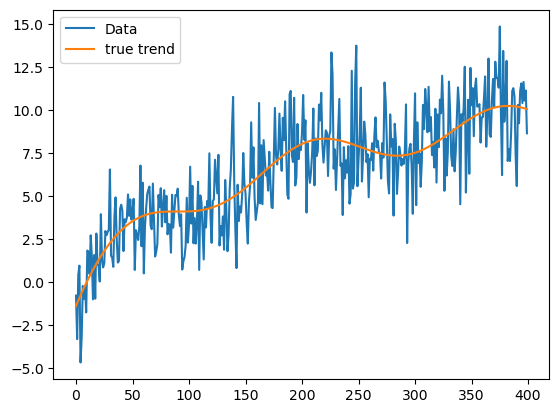

Next we consider a simulated dataset that is obtained by adding noise to a smooth trend function.

def smoothfun(x):

ans = np.sin(15*x) + 3*np.exp(-(x ** 2)/2) + 0.5*((x - 0.5) ** 2) + 5 * np.log(x + 0.1) + 7

return ans

n = 400

xx = np.linspace(0, 1, 400)

truth = np.array([smoothfun(x) for x in xx])

sig = 2

rng = np.random.default_rng(seed = 42)

errorsamples = rng.normal(loc=0, scale = sig, size = n)

y = truth + errorsamples

plt.plot(y, label = 'Data')

plt.plot(truth, label = 'true trend')

plt.legend()

plt.show()

n = len(y)

x = np.arange(1, n+1)

Xfull = np.column_stack([np.ones(n), x-1])

for i in range(n-2):

c = i+2

xc = ((x > c).astype(float))*(x-c)

Xfull = np.column_stack([Xfull, xc])

print(Xfull)[[ 1. 0. -0. ... -0. -0. -0.]

[ 1. 1. 0. ... -0. -0. -0.]

[ 1. 2. 1. ... -0. -0. -0.]

...

[ 1. 397. 396. ... 1. 0. -0.]

[ 1. 398. 397. ... 2. 1. 0.]

[ 1. 399. 398. ... 3. 2. 1.]]

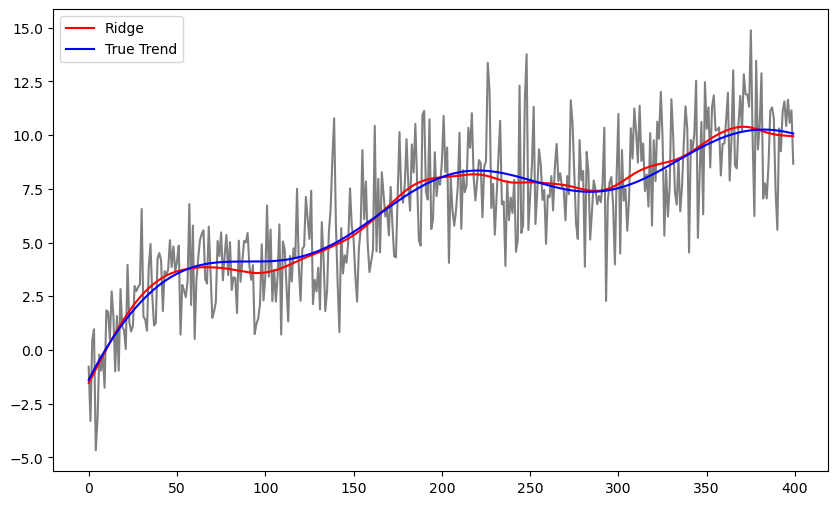

b_ridge = solve_ridge(Xfull, y, lambda_val = 10000)

ridge_fitted = np.dot(Xfull, b_ridge)

plt.figure(figsize = (10, 6))

plt.plot(y, color = 'gray')

plt.plot(ridge_fitted, color = 'red', label = 'Ridge')

plt.plot(truth, color = 'blue', label = "True Trend")

plt.legend()

plt.show()

lambda_candidates = np.array([10, 100, 1000, 10000, 100000, 1000000])

best_lambda, cv_errors = ridge_cv(Xfull, y, lambda_candidates)

print(best_lambda)

print("CV errors for each lambda:")

for lamb, error in sorted(cv_errors.items()):

print(f"Lambda = {lamb:.2f}, CV Error = {error:.6f}")

100000

CV errors for each lambda:

Lambda = 10.00, CV Error = 4.221263

Lambda = 100.00, CV Error = 4.052517

Lambda = 1000.00, CV Error = 3.894083

Lambda = 10000.00, CV Error = 3.791721

Lambda = 100000.00, CV Error = 3.771729

Lambda = 1000000.00, CV Error = 3.970162

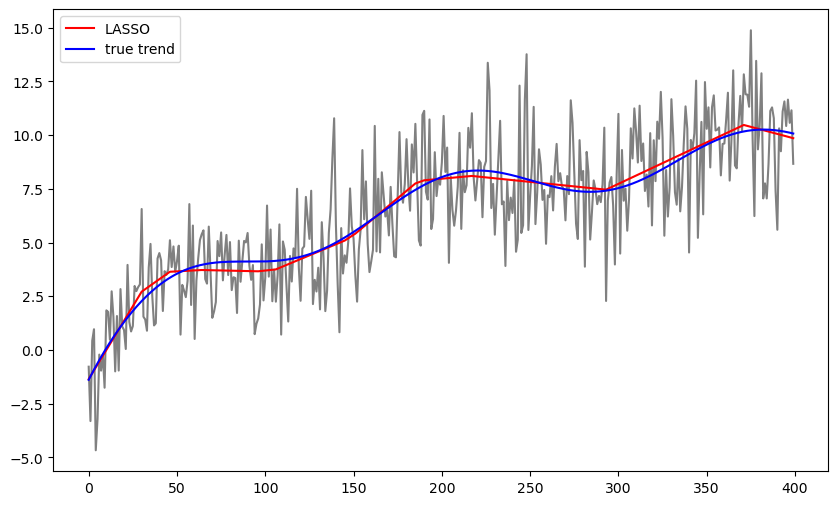

b_lasso = solve_lasso(Xfull, y, lambda_val = 100)

lasso_fitted = np.dot(Xfull, b_lasso)

plt.figure(figsize = (10, 6))

plt.plot(y, color = 'gray')

plt.plot(lasso_fitted, color = 'red', label = 'LASSO')

plt.plot(truth, color = 'blue', label = "true trend")

plt.legend()

plt.show()

lambda_candidates = np.array([1, 10, 100, 1000, 10000])

best_lambda, cv_errors = lasso_cv(Xfull, y, lambda_candidates)

print(best_lambda)

print("CV errors for each lambda:")

for lamb, error in sorted(cv_errors.items()):

print(f"Lambda = {lamb:.3f}, CV Error = {error:.6f}")100

CV errors for each lambda:

Lambda = 1.000, CV Error = 4.596651

Lambda = 10.000, CV Error = 4.084715

Lambda = 100.000, CV Error = 3.809634

Lambda = 1000.000, CV Error = 4.027127

Lambda = 10000.000, CV Error = 4.378784

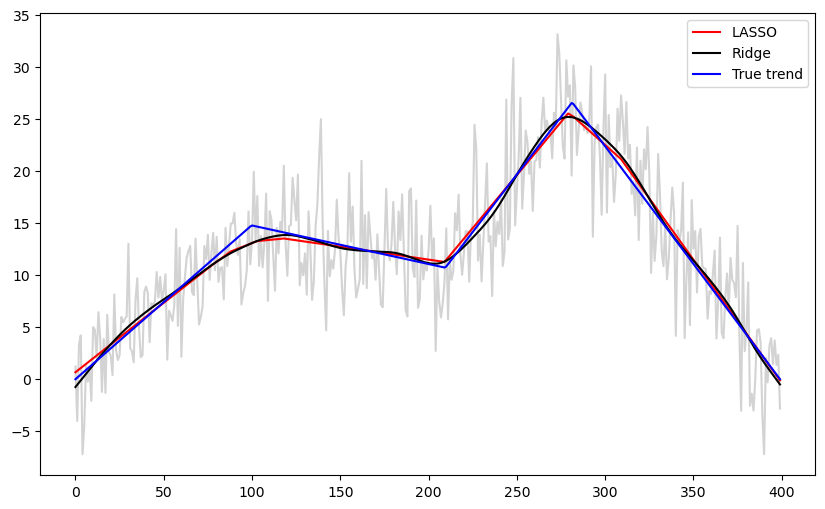

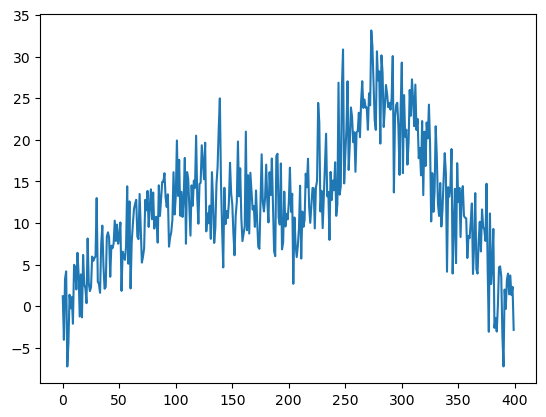

The following code considers simulated data from a piecewise linear trend function corrupted with noise.

def piece_linear(x):

ans = np.zeros_like(x, dtype=float)

# First segment: 0 <= x <= 0.25

mask1 = (x >= 0) & (x <= 0.25)

ans[mask1] = (14.77491 / 0.25) * x[mask1]

# Second segment: 0.25 < x <= 0.525

mask2 = (x > 0.25) & (x <= 0.525)

ans[mask2] = (10.71181 + ((10.71181 - 14.77491) / (0.525 - 0.25)) * (x[mask2] - 0.525))

# Third segment: 0.525 < x <= 0.705

mask3 = (x > 0.525) & (x <= 0.705)

ans[mask3] = (26.59484 + ((26.59584 - 10.71181) / (0.705 - 0.525)) * (x[mask3] - 0.705))

# Fourth segment: 0.705 < x <= 1

mask4 = (x > 0.705) & (x <= 1)

ans[mask4] = ((0 - 26.59584) / (1 - 0.705)) * (x[mask4] - 1)

return ans

n = 400

xx = np.linspace(0, 1, 400)

truth = piece_linear(xx)

sig = 4

rng = np.random.default_rng(seed = 42)

errorsamples = rng.normal(loc=0, scale = sig, size = n)

y = truth + errorsamples

plt.plot(y)

plt.show()

n = len(y)

x = np.arange(1, n+1)

Xfull = np.column_stack([np.ones(n), x-1])

for i in range(n-2):

c = i+2

xc = ((x > c).astype(float))*(x-c)

Xfull = np.column_stack([Xfull, xc])

print(Xfull)[[ 1. 0. -0. ... -0. -0. -0.]

[ 1. 1. 0. ... -0. -0. -0.]

[ 1. 2. 1. ... -0. -0. -0.]

...

[ 1. 397. 396. ... 1. 0. -0.]

[ 1. 398. 397. ... 2. 1. 0.]

[ 1. 399. 398. ... 3. 2. 1.]]

lambda_candidates = np.array([1000, 10000, 100000, 1000000])

best_lambda, cv_errors = ridge_cv(Xfull, y, lambda_candidates)

print(best_lambda)

print("CV errors for each lambda:")

for lamb, error in sorted(cv_errors.items()):

print(f"Lambda = {lamb:.2f}, CV Error = {error:.6f}")

10000

CV errors for each lambda:

Lambda = 1000.00, CV Error = 15.604092

Lambda = 10000.00, CV Error = 15.223786

Lambda = 100000.00, CV Error = 15.340427

Lambda = 1000000.00, CV Error = 18.374224

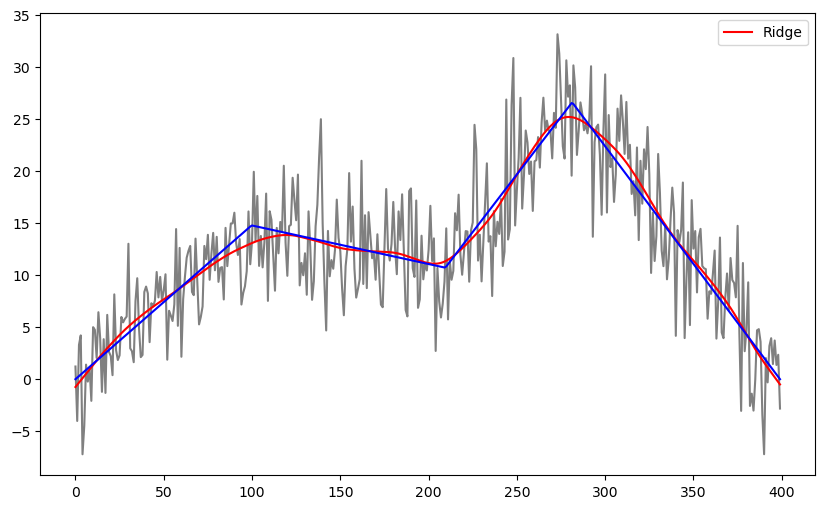

b_ridge = solve_ridge(Xfull, y, lambda_val = 10000)

ridge_fitted = np.dot(Xfull, b_ridge)

plt.figure(figsize = (10, 6))

plt.plot(y, color = 'gray')

plt.plot(ridge_fitted, color = 'red', label = 'Ridge')

plt.plot(truth, color = 'blue')

plt.legend()

plt.show()

lambda_candidates = np.array([1, 10, 100, 1000, 10000])

best_lambda, cv_errors = lasso_cv(Xfull, y, lambda_candidates)

print(best_lambda)

print("CV errors for each lambda:")

for lamb, error in sorted(cv_errors.items()):

print(f"Lambda = {lamb:.3f}, CV Error = {error:.6f}")1000

CV errors for each lambda:

Lambda = 1.000, CV Error = 19.302664

Lambda = 10.000, CV Error = 16.938073

Lambda = 100.000, CV Error = 15.228507

Lambda = 1000.000, CV Error = 15.180670

Lambda = 10000.000, CV Error = 22.089595

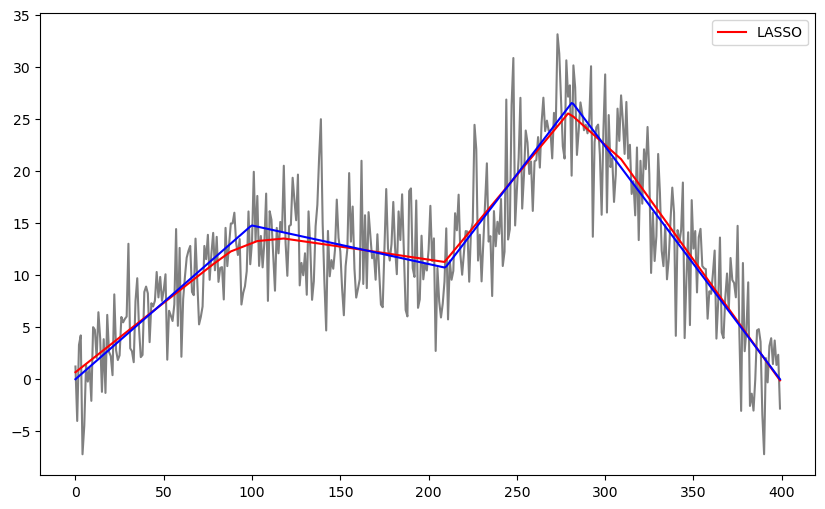

b_lasso = solve_lasso(Xfull, y, lambda_val = 1000)

lasso_fitted = np.dot(Xfull, b_lasso)

plt.figure(figsize = (10, 6))

plt.plot(y, color = 'gray')

plt.plot(lasso_fitted, color = 'red', label = 'LASSO')

plt.plot(truth, color = 'blue')

plt.legend()

plt.show()

b_ridge = solve_ridge(Xfull, y, lambda_val = 10000)

ridge_fitted = np.dot(Xfull, b_ridge)

b_lasso = solve_lasso(Xfull, y, lambda_val = 1000)

lasso_fitted = np.dot(Xfull, b_lasso)

plt.figure(figsize=(10, 6))

plt.plot(y, color = 'lightgray')

#plt.plot(y, color = 'None')

plt.plot(lasso_fitted, color = 'red', label = 'LASSO')

plt.plot(ridge_fitted, color = 'black', label = "Ridge")

plt.plot(truth, color = 'blue', label = 'True trend')

plt.legend()

plt.show()