import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import statsmodels.api as sm

from statsmodels.tsa.ar_model import AutoReg

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

Sample PACF¶

Towards the end of last lecture, we discussed the Sample PACF (Partial Autocorrelation Function) that is used as an exploratory data analysis tool mainly for determining an appropriate order for fitting the AR() model to the data. The sample PACF at lag is simply equal to the esimate of when an AR() model is fit to the data. We also discussed briefly why this quantity (obtained by fitting AR() models for various is has “partial autocorrelation” in its name). You will revisit this again in tomorrow’s lab.

Now, we shall show code for calculating the sample PACF. We shall calculate it directly by fitting AR(p) models with increasing . We shall also use inbuilt functions from statsmodels to compute the sample PACF, and we will verify that we are getting exactly the same answers.

Let us use the GNP dataset that was previously used in Lab 10.

gnp = pd.read_csv("GNP_02April2025.csv")

print(gnp.head())

y = gnp['GNP']

plt.figure(figsize = (12, 6))

plt.plot(y, color = 'black')

plt.show() observation_date GNP

0 1947-01-01 244.142

1 1947-04-01 247.063

2 1947-07-01 250.716

3 1947-10-01 260.981

4 1948-01-01 267.133

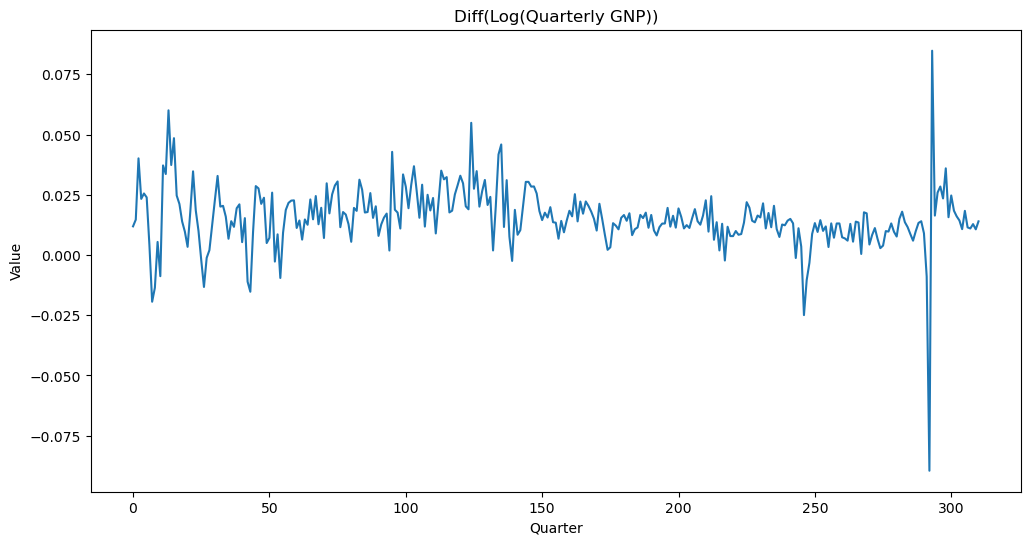

Instead of working with the GNP data directly, we shall first take logarithms and then differences.

ylogdiff = np.diff(np.log(y))

plt.figure(figsize = (12, 6))

plt.plot(ylogdiff)

plt.title('Diff(Log(Quarterly GNP))')

plt.ylabel('Value')

plt.xlabel('Quarter')

plt.show()

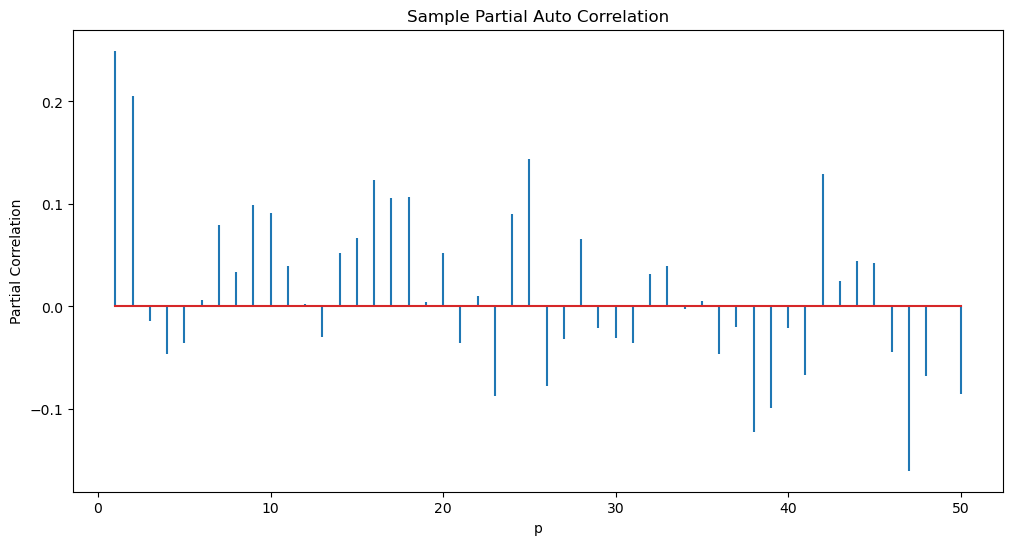

Suppose we want to fit an AR() model to this dataset. What is a suitable value of ? To figure this out, we can simply compute the sample PACF.

def sample_pacf(y, p_max):

pautocorr = []

for p in range(1, p_max + 1):

armd = AutoReg(ylogdiff, lags = p).fit()

phi_p = armd.params[-1]

pautocorr.append(phi_p)

return pautocorr

p_max = 50

sample_pacf_vals = sample_pacf(ylogdiff, p_max)

plt.figure(figsize = (12, 6))

markerline, stemline, baseline = plt.stem(range(1, p_max + 1), sample_pacf_vals)

markerline.set_marker("None")

plt.xlabel("p")

plt.ylabel('Partial Correlation')

plt.title("Sample Partial Auto Correlation")

plt.show()

Next let us use an inbuilt function from statsmodels to compute the pacf.

from statsmodels.tsa.stattools import pacf

pacf_values = pacf(ylogdiff, nlags=p_max, method = 'ols')

print(np.column_stack([sample_pacf_vals, pacf_values[1:]])) #check that these values match exactly [[ 0.2494903 0.2494903 ]

[ 0.20501251 0.20501251]

[-0.01395884 -0.01395884]

[-0.04624678 -0.04624678]

[-0.03576291 -0.03576291]

[ 0.00612623 0.00612623]

[ 0.07954096 0.07954096]

[ 0.03379382 0.03379382]

[ 0.09908671 0.09908671]

[ 0.09148765 0.09148765]

[ 0.03935477 0.03935477]

[ 0.00231935 0.00231935]

[-0.02952129 -0.02952129]

[ 0.05181593 0.05181593]

[ 0.0668389 0.0668389 ]

[ 0.12328399 0.12328399]

[ 0.10611304 0.10611304]

[ 0.10657613 0.10657613]

[ 0.0044102 0.0044102 ]

[ 0.05242979 0.05242979]

[-0.03582163 -0.03582163]

[ 0.01026383 0.01026383]

[-0.08690484 -0.08690484]

[ 0.09000221 0.09000221]

[ 0.1440655 0.1440655 ]

[-0.07755717 -0.07755717]

[-0.03216266 -0.03216266]

[ 0.06553052 0.06553052]

[-0.02122327 -0.02122327]

[-0.03054263 -0.03054263]

[-0.03595624 -0.03595624]

[ 0.03193371 0.03193371]

[ 0.03931399 0.03931399]

[-0.00235186 -0.00235186]

[ 0.00512543 0.00512543]

[-0.04618897 -0.04618897]

[-0.0203755 -0.0203755 ]

[-0.12254506 -0.12254506]

[-0.09938421 -0.09938421]

[-0.02095841 -0.02095841]

[-0.06731694 -0.06731694]

[ 0.12911652 0.12911652]

[ 0.02500216 0.02500216]

[ 0.04445531 0.04445531]

[ 0.04253399 0.04253399]

[-0.04416781 -0.04416781]

[-0.16020234 -0.16020234]

[-0.06809175 -0.06809175]

[ 0.00068818 0.00068818]

[-0.08538738 -0.08538738]]

In comparison to our plot of the sample_pacf values, the inbuilt sample_pacf plot from statsmodels will look slightly different (even though it is plotting the same values). The differences are: (a) it also plots the value 1 at lag 0, (b) it gives a shaded region that can be used to assess whether values are negligible or not.

fig, axes = plt.subplots(figsize = (12, 6))

plot_pacf(ylogdiff, lags = p_max, ax = axes)

axes.set_title("Sample PACF of diff_log_GDP Series")

plt.show()

From the above plot, it appears that AR(2) is a good model for this dataset.

ar2 = AutoReg(ylogdiff, lags = 2).fit()

print(ar2.summary()) AutoReg Model Results

==============================================================================

Dep. Variable: y No. Observations: 311

Model: AutoReg(2) Log Likelihood 921.191

Method: Conditional MLE S.D. of innovations 0.012

Date: Fri, 11 Apr 2025 AIC -1834.381

Time: 13:06:41 BIC -1819.448

Sample: 2 HQIC -1828.411

311

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0092 0.001 7.289 0.000 0.007 0.012

y.L1 0.1984 0.056 3.563 0.000 0.089 0.307

y.L2 0.2050 0.056 3.682 0.000 0.096 0.314

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.7771 +0.0000j 1.7771 0.0000

AR.2 -2.7447 +0.0000j 2.7447 0.5000

-----------------------------------------------------------------------------

Another way of fitting AR models in statsmodels is to use the ARIMA function, as shown below.

from statsmodels.tsa.arima.model import ARIMA

ar2_arima = sm.tsa.arima.ARIMA(ylogdiff, order = (2, 0, 0)).fit() #order = (2, 0, 0) refers to the AR(2) model.

print(ar2_arima.summary()) SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 311

Model: ARIMA(2, 0, 0) Log Likelihood 928.043

Date: Fri, 11 Apr 2025 AIC -1848.087

Time: 13:06:46 BIC -1833.128

Sample: 0 HQIC -1842.108

- 311

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0154 0.001 10.694 0.000 0.013 0.018

ar.L1 0.1981 0.026 7.683 0.000 0.148 0.249

ar.L2 0.2036 0.068 2.996 0.003 0.070 0.337

sigma2 0.0001 3.88e-06 38.544 0.000 0.000 0.000

===================================================================================

Ljung-Box (L1) (Q): 0.00 Jarque-Bera (JB): 7805.10

Prob(Q): 0.96 Prob(JB): 0.00

Heteroskedasticity (H): 1.61 Skew: -0.07

Prob(H) (two-sided): 0.02 Kurtosis: 27.54

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Note that the estimates computed by the ARIMA function are slightly different from the estimates computed by the “conditional MLE” method in AutoReg. There are many methods that are used by these functions. Generally they all should give similar answers.

help(ARIMA)AR(1) with ¶

Consider the model:

for some with absolute value strictly larger than 1. This is the non-causal AR model.

Let us attempt to simulate data from this model. It is most natural to simulate this for decreasing (there might be numerical issues with trying to simulate this in the usual way for with increasing ).

phi1 = 2

sig = 3

mu = 10

n = 2000

nf = 50 #number of future epsilons that we generate

rng = np.random.default_rng(seed = 43)

eps = rng.normal(loc = 0, scale = sig, size = n + nf)

yn = mu

for i in range(1, nf):

yn = yn - eps[n+i-1]/(phi1 ** i)

print(yn)

y = np.full(n, -999, dtype = float)

y[-1] = yn

for t in range(n-1, 0, -1):

y[t-1] = (y[t]/phi1) - (mu*(1-phi1)/phi1) - eps[t]/phi1

print(y)

plt.figure(figsize = (12, 6))

plt.plot(y)

plt.show()10.263896524224691

[10.0395212 12.11357735 12.47056656 ... 7.74365861 9.23878741

10.26389652]

ar = ARIMA(y, order = (1, 0, 0)).fit()

print(ar.summary()) SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 2000

Model: ARIMA(1, 0, 0) Log Likelihood -3638.593

Date: Fri, 11 Apr 2025 AIC 7283.187

Time: 13:07:18 BIC 7299.990

Sample: 0 HQIC 7289.356

- 2000

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 10.0199 0.062 162.683 0.000 9.899 10.141

ar.L1 0.4581 0.020 23.121 0.000 0.419 0.497

sigma2 2.2268 0.070 31.870 0.000 2.090 2.364

===================================================================================

Ljung-Box (L1) (Q): 0.10 Jarque-Bera (JB): 0.23

Prob(Q): 0.75 Prob(JB): 0.89

Heteroskedasticity (H): 0.99 Skew: 0.02

Prob(H) (two-sided): 0.92 Kurtosis: 3.03

===================================================================================

Warnings:

[1] Covariance matrix calculated using the outer product of gradients (complex-step).

Note that the estimate of in the above regression is 0.4581 which is quite far from the actual used to generate the data. Also note that the estimate of is 2.2268 while the actual .